8.9.18

Correction time: The market takes a hit

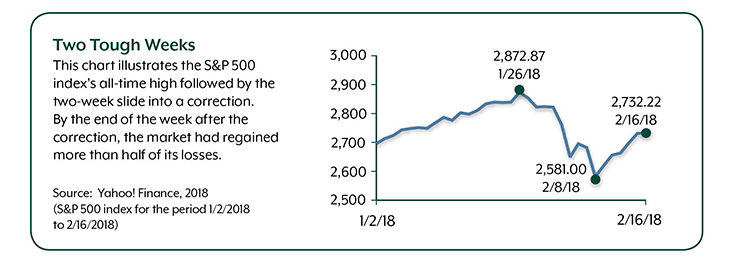

After reaching all-time highs on January 26, 2018, the Dow Jones Industrial Average and the S&P 500 went into a two-week slide that saw both stock indexes drop by more than 10%, a decline that is typically considered a market correction.1

Analysts have been saying for several years that the long, booming bull market was overvalued and due for a correction, so the drop was not a surprise in the big picture.2 And even after the 10% plunge, the Dow was up 19% over the previous 12 months, and the S&P 500 was up 12.5%.3

It’s natural to be concerned about this kind of shift, but more important to maintain perspective and focus on your long-term goals. It may be helpful to consider some of the reasons behind the surge of market volatility.

Too Much of a Good Thing?

The initial trigger for the downturn was a better-than-expected jobs report on February 2 that helped drive the Dow down more than 2.5%, a significant decline considering the unusually low volatility in 2017 and the beginning of 2018. The economy added 200,000 jobs in January, marking the 88th straight month of job creation, the longest such run in U.S. history. Wages rose by 2.9% over the previous January, the highest year-over-year increase since the end of the recession in June 2009. And the unemployment rate held steady at 4.1% for the fourth straight month, the lowest level in 17 years.4

Although the report was great news for U.S. workers, on Wall Street the rosy jobs picture generated fears of higher inflation that might drive the Federal Reserve to raise interest rates more quickly than anticipated. At its December 2017 meeting, the Federal Open Market Committee signaled its intention to raise the benchmark federal funds rate three times in 2018, bringing it up to a range of 2.0% to 2.25%. Theoretically, these changes have been priced into the market, but the strong jobs report made it more likely that the Fed will follow through on its projection and possibly execute further increases if inflation heats up.5

Stocks, Bonds, and U.S. Debt

Higher interest rates rattle the stock market because investors are more likely to move assets out of risky stocks and into more stable bonds, as fixed-income yields become more attractive. Higher rates not only mean increased yields on new bonds but also on existing bonds, as prices are pushed downward to make yields competitive. In addition, the prospect of inflation tends to push bond prices lower and yields higher, because inflation erodes the purchasing power of fixed-income payments.

One reason for the initial reaction to the January jobs report expanding into a full-blown correction is that bond yields were already rising due to other factors. The yield on the 10-year Treasury note — a bedrock of global financial markets — has been rising since tax legislation was proposed in the fall of 2017, and the yield reached a four-year high of 2.85% on the day the jobs report was released.6–7 Although the Tax Cuts and Jobs Act was generally welcomed on Wall Street, bond traders have been concerned that increased Treasury sales to pay for the $1.5 trillion tax cuts will erode bond prices. This concern was exacerbated by the bipartisan budget deal that further increased deficit spending.8

The Treasury is working to finance higher debt at the same time the Federal Reserve is unwinding its recession-era bond-buying program. With the Fed reducing its bond portfolio, the Treasury must sell more bonds to the public to cover growing deficits. The Treasury recently announced the first increase in bond sales since 2009.9

The question is who will buy these bonds and what are they willing to pay for them? A weak dollar has made Treasuries less appealing to foreign governments, which hold more than 44% of U.S. government debt. With the Treasury market depending more on U.S. investors, supply may be outpacing demand — illustrated by a tepid Treasury auction on February 7.10

The Long View

Although mounting government debt is a serious concern, the stock and bond markets are both driven in the long term by the economy, and the United States looks to be hitting its stride after a long, slow recovery. The global economy, which has been even slower to recover, is coming back as well.

A correction may be disturbing, but it can strengthen the market in the long term by returning equity values to levels that are more in line with corporate earnings and less dependent on investor exuberance. A corrected market may also be less vulnerable to overreaction. On February 14, the Dow and the S&P 500 closed up more than 1.2%, despite a consumer report that showed higher-than-expected inflation. Even with higher prices in January, core inflation (which excludes food and energy prices) is running at only 1.8%, still below the Fed’s 2% target rate.11

Of course, no one can predict the future, and you might see volatility for some time. The wisest course may be to remain patient and avoid making portfolio decisions based on emotion.

The return and principal value of stocks and bonds fluctuate with changes in market conditions. Shares, when sold, and bonds redeemed prior to maturity may be worth more or less than their original cost. U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest.

The S&P 500 is an unmanaged group of securities that is considered representative of the U.S. stock market in general. The performance of an unmanaged index is not indicative of the performance of any specific investment. Individuals cannot invest directly in an index. Past performance is no guarantee of future results. Actual results will vary.

1, 3) Yahoo! Finance, 2018 (Dow Jones Industrial Average and S&P 500 index for the period 2/8/2017 to 2/8/2018)

2) Bloomberg, February 6, 2018

4–5) The Wall Street Journal, February 2, 2018

6) CNBC, January 11, 2018

7) CNNMoney, February 2, 2018

8) MarketWatch, February 12, 2018

9) Bloomberg, January 31, 2018

10) Bloomberg, February 7, 2018

11) MarketWatch, February 14, 2018

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2018 Broadridge Investor Communication Solutions, Inc.

* Non-deposit investment products and services are offered through CUSO Financial Services, L.P. (“CFS”), a registered broker-dealer (Member FINRA/SIPC) and Registered Investment Advisor. Products offered through CFS: are not NCUA/NCUSIF or otherwise federally insured, are not guarantees or obligations of the credit union, and may involve investment risk including possible loss of principal. Investment Representatives are registered through CFS. Consumers Credit Union has contracted with CFS to make non-deposit investment products and services available to credit union members.